The 4% Retirement Planning Rule is an important process to obtain financial security after retirement. By understanding this rule you could easily understand how much you can withdraw from your retirement corpus so as to ensure you do not have scarcity of funds after retirement. Let us understand this 4% retirement planning rule.

People follow the process of retirement planning to ensure the respectable evening of life, to ensure the sufficiency of funds for basic needs if they are unable to earn when the age factor comes into force.

Some invest in PPF, some invest in EPF and some other invest in NPS. But knowingly this 4% retirement planning rule you could ensure the success of your retirement plans.

This 4% retirement planning rule tells you about how much you can withdraw each year from your retirement corpus to ensure a sufficient bank balance.

The best part of this rule is you could see your corpus increasing every year even if you are withdrawing a sufficient amount every year for your needs and wants.

What is 4% Retirement Planning Rule

This 4% retirement planning rule was given by an American financial advisor “Bill Bengen” in mid-1990’s.

The purpose of his research was to find out how much a person could withdraw from his retirement corpus so that he couldn’t face shortage of funds after retirement.

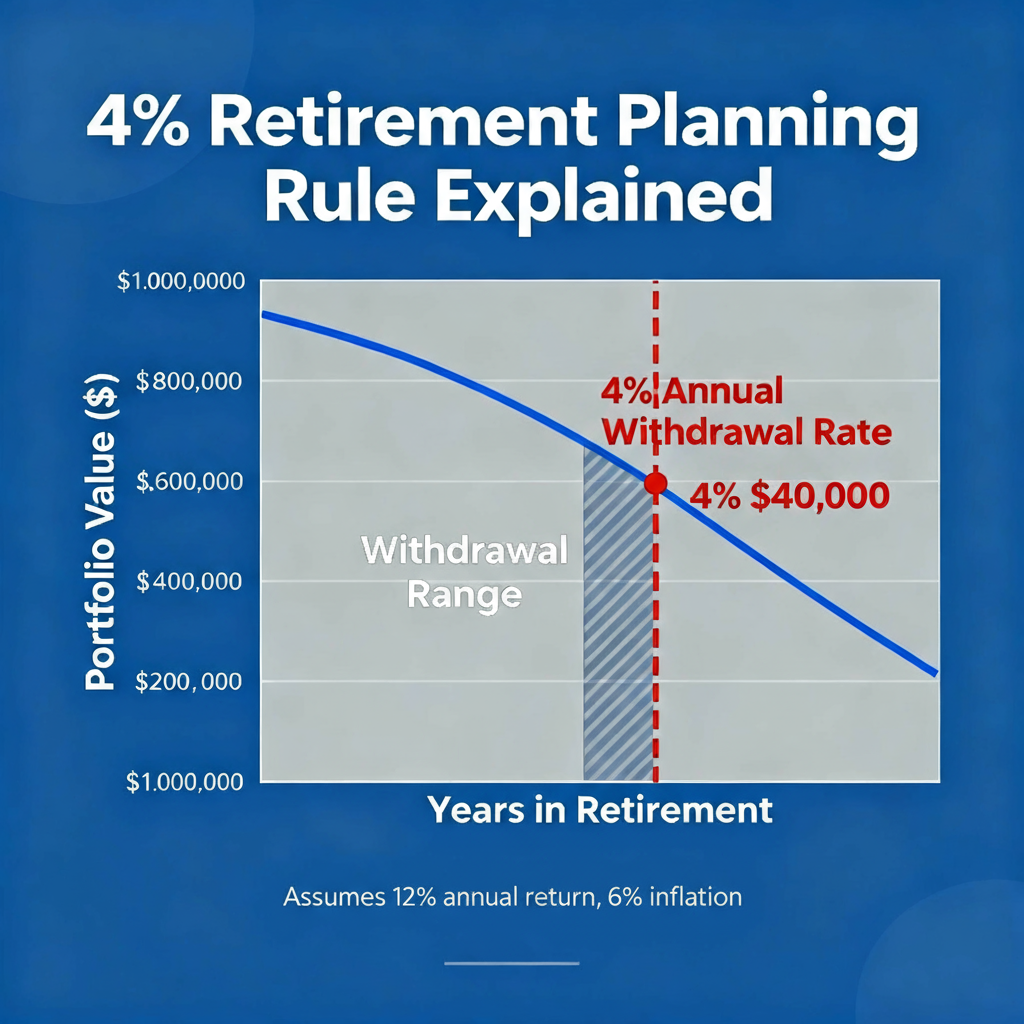

4% retirement planning rule says that a retired person should withdraw up to 4% per year from his retirement corpus if he wants to ensure sufficiency of funds after his retirement when he is not earning but only expending.

4% Retirement Planning Rule Might Increase Corpus

Yes you read it right, the 4% retirement planning rule could actually increase your retirement corpus if you take some smart decisions. Let us understand by an example:

Example:

Suppose you have retirement corpus of RS 5 crore, you withdraw 4% each year (assuming inflation at 6%, therefore you are also increasing the withdrawal percentage each year so as to price in the effect of inflation) and you know the investment avenues which could give you 12% return per year.

So at the end of first year you would have corpus of 5,37,60,000 even if you withdraw 20 lakh (4% of 5 crore) at the beginning of first year after retirement.

At the end of second year you would have 5,78,36,800 even if you withdraw 21,20,000 (adjusting the withdrawal amount by inflation, therefore the withdrawal increased so as to price in the inflation).

Similarly at the end of 30th year you would still have 5,93,91,600 even if you had withdrawn 4% each year after adjusting inflation (.i.e. increase your withdrawal amount equal to inflation figure of 6%).

So if you retired at 60 years of age, with proper retirement planning, all your financial needs are taken care of for at least next 30 years.

This shows that your corpus has actually increased if you have planned properly.

Steps For Retirement Planning

Step One: Understand Your Retirement Corpus

First step to create retirement corpus is to identify how much money do you need as the retirement corpus.

This has to be planned on the basis of your yearly expenses after retirement. It depends upon your lifestyle. Now let’s suppose as of today you came to know that a retired person having monthly expenditure of Rs 80,000 could live a life as per your standard of living.

Now adjust Rs 80,000 for 6% inflation per year, then this Rs 80,000 will become approximately Rs 2,50,000 after 20 years. It means you need approximately Rs 30,00,000 per year (Rs 2,00,000 x 12) after your retirement.

Step Two: Multiply Yearly Expenditure By 25

Now multiply this Rs 30,00,000 by 25. But, what is the logic to multiply it by 25?

The logic came from our 4% rule. If your withdraw 4% per year then your corpus will remain for approximately 25 years after your retirement therefore if you multiply Rs 30,00,000 with 25 the approximate retirement corpus you need would be Rs 7,50,00,000 (.i.e. Expenditure for 1 year multiply by 25, this will give the amount of expenditure required for next 25 years)

Step Three: Calculate the Withdrawal Amount for The First Year After Retirement

As per our 4% retire planning rule withdraw 4% of Rs 7,50,00,000 for the first year .i.e. Rs 30,00,000 for the first year. This would be sufficient to cover your entire expenses for the first year as we discussed in Step 1 above.

Let the remaining amount invested in the instruments wherein you could get higher returns.

Step Four: Calculate The Withdrawal Amount For The Subsequent Years After Retirement

Increase the withdrawal amount as per the inflation. Suppose the inflation is 6% then in the second year you have to withdraw Rs 30,00,000 plus 6% of Rs 30,00,000 .i.e. Rs 30,00,000 + Rs 1,80,000 .i.e. Rs 31,80,000 this increment will help you in maintaining the same lifestyle even if the inflation has increased in the next year.

In the third year again increase Rs30,00,000 by another 6% so as to price in the inflation. Carry on the same way for subsequent years.

Why This 4% Retirement Planning Rule is So Important

It is the safe and stable way to live a peaceful and stress-free retired life. It helps in attaining a planned corpus and enforce the person to save for the retirement.

When you have a written plan and a specific target to achieve, you become disciplined towards achieving your goals.

It prevents you from doing extravagant expenditures and motivates you to save more so as to achieve the desired retirement corpus.

What if You are Earning Even After Retirement

If you are still earning after retirement then you should tweak your withdrawals towards lower side so that you could accumulate smart corpus and transfer it as a legacy for next generations.

Timely Review of Retirement Plans

Most common mistake that people usually do is they do not review their retirement investment portfolio after retirement. It is advised to regularly review the investment portfolio if the market sentiments are changing or interest rates are reducing.

You should again tweak your withdrawals so as to ensure the sufficient capital remaining in your account.

Final Words

Never under estimate the power of retirement planning because you will need the money even if you are not earning.

But, from where would you get the retirement corpus? It is only through planning during your service tenure or when you are young.

4% retirement planning tool is not a miracle but it is a reward for those who plan for their future.

Planning save you from being dependent on your kids or any other person. You would live a peaceful and respectable retired life. What you need is just a disciplined, well advised retirement plan prepared with the help of your financial advisor.

Great read…..